-

-

North

-

Midlands & East

-

London

-

South West

-

North

Midlands & East

London

South West

Before you continue

Generic error message

The selected items have been added to your basket

View BasketYour Basket will expire in time minutes.

1. DEFINITIONS

|

AVCs |

Additional Voluntary Contributions |

|

ESG |

Environmental, Social and Governance |

|

Investment Adviser |

The Trustees are advised on investment matters by First Actuarial LLP. First Actuarial LLP is regulated by the Institute and Faculty of Actuaries and is qualified to provide the required advice through knowledge and practical experience of financial matters relating to pension schemes. |

|

Legislation |

This statement has been drafted to comply with relevant legislation. In particular, consideration has been given to: · the Pensions Act 1995; · the Occupational Pensions (Investment) Regulations 2005; · the Pension Protection Fund (Pensionable Service) and Occupational Pension Schemes (Investment and Disclosure) (Amendment and Modification) Regulations 2018; and · the Occupational Pension Schemes (Investment and Disclosure) (Amendment) Regulations 2019. |

|

Scheme |

Jockey Club Racecourses Pension Scheme |

|

Trustees |

The Trustees of the Scheme |

This statement is made in accordance with the requirements of legislation. The main body of the document sets out the principles and policies that govern investments made by the Trustees whilst details of the specific investment arrangements in place are provided in the Appendix.

Throughout the statement, wording in bold represents actions that will be taken by the Trustees in the implementation and monitoring of the Scheme’s investment arrangements.

Investment advice

The Trustees received and considered written investment advice from the Investment Adviser to help with the preparation of this statement.

The Trustees will obtain and consider written advice from the Investment Adviser when reviewing the Scheme’s investment strategy or when considering the suitability of potential investments. The Trustees expect that such advice will be consistent with any guidance issued by The Pensions Regulator.

Legal advice

The Trustees will seek legal advice relating to investment matters whenever deemed necessary.

Consultation with the sponsoring employer

In preparing this statement, the Trustees consulted with the sponsoring employer.

The Trustees will consult with the sponsoring employer before making any changes to the Scheme’s investment strategy.

Conflicts of interest

The Trustees are satisfied that the Scheme’s investment strategy meets their responsibility to invest the assets in the best interests of the members and beneficiaries and, in the case of a potential conflict of interest, in the sole interest of the members and beneficiaries.

The investment beliefs stated below have been developed by the Trustees and are reflected in the Scheme’s investment strategy.

Basic investment principles

The Trustees believe that the following three basic investment principles should be taken into account in the construction of the Scheme’s investment strategy:

Financially material considerations and the appropriate time horizon

The Trustees believe that the potential impact of any financially material considerations that may affect the Scheme’s investments should be assessed over the period during which benefits are expected to be paid from the Scheme. In the terminology used by legislation, the Trustees consider this period of time to be “the appropriate time horizon of the investments”.

ESG

The Trustees believe that the impact of ESG risks and opportunities can be financially material and the Trustees recognise that ESG matters, particularly climate change, should be assessed over the appropriate time horizon.

Use of active management

The Trustees believe that active management has the potential to add value either through offering the prospect of enhanced returns or through the control of volatility.

The Trustees believe that active management may help to mitigate the financial impact of ESG risks.

Stewardship

The Trustees believe that good stewardship can help create, and preserve, value for companies and markets as a whole.

Members’ views (non-financial matters)

Legislation defines non-financial matters as meaning the views of the members and beneficiaries including (but not limited to) ESG matters and the present and future quality of life of the members and beneficiaries of the Scheme.

The Trustees believe that their duty to members and beneficiaries will be best served by ensuring that all benefits can be paid as they fall due and the Trustees’ Investment Objectives are designed to ensure this duty is achieved.

In reaching this conclusion, the Trustees considered whether to take members’ views into account when determining a suitable investment strategy and in the selection, retention and realisation of investments. However, the Trustees have determined that it would not be practical to do so. In particular, the Trustees concluded that it is likely that members and beneficiaries would hold a broad range of views, which would be difficult to accommodate.

At least every three years, the Trustees will:

The Trustees’ primary investment objectives are:

The Trustees’ investment approach is designed to strike a balance between the above primary objectives but also considers:

The Trustees have taken advice from the Investment Adviser to construct a portfolio of investments consistent with these objectives. In doing so, consideration is given to all matters which are believed to be financially material.

Details of the current investment strategy are provided in the Appendix.

The Trustees will review their investment objectives and the Scheme’s strategic asset allocation at least every three years.

Types of investments to be held

The Trustees are permitted to invest across a wide range of asset classes, including, but not limited to, the following:

Use of pooled funds

Day-to-day management of the Scheme’s assets, including the selection, retention and realisation of investments, is delegated to one or more investment managers. When the Trustees require funds to meet cashflows, one or more of their investment managers will be instructed to make a disinvestment.

Taking into account the size of the Scheme’s assets, the Trustees have concluded that pooled funds represent the most pragmatic way of implementing the Scheme’s investment strategy rather than establishing segregated mandates with investment managers.

To ensure safekeeping of the assets, ownership and day-to-day control of the assets is undertaken by custodian organisations which are independent of the sponsoring employer and the investment managers. Where a pooled fund is held, the custodian will typically be appointed by the investment manager.

The assets held by the Scheme are invested predominantly on regulated markets, as so defined in legislation. Any investments that do not trade on regulated markets are kept to a prudent level.

The Trustees will primarily hold pooled funds and will ensure the Scheme’s assets are predominantly invested on regulated markets.

Use of derivatives

The Trustees may select pooled funds which are permitted to use derivative instruments to reduce risk or for efficient portfolio management. Risk reduction would include mitigating the impact of a potential fall in markets or the implementation of currency hedging whilst efficient portfolio management would include using derivatives as a cost-effective way of gaining access to a market or as a method for generating capital and/or income with an acceptable level of risk.

Leverage

Investments held to match the sensitivity of the Scheme’s liabilities to changes in interest rates and inflation may be leveraged. The use of such assets can reduce the volatility of the Scheme’s funding position.

Alignment with the Trustees’ investment principles

As the Scheme’s assets are held in pooled funds, the Trustees have limited influence over the investment managers’ investment decisions. In practice, investment managers cannot fully align their strategy and decisions to the (potentially conflicting) policies of all their pooled fund investors in relation to strategy, long-term performance of debt/equity issuers, engagement and portfolio turnover.

It is therefore the Trustees’ responsibility to ensure that the approaches adopted by investment managers are consistent with the Trustees’ policies before any new appointment, and to monitor and to consider terminating any existing arrangements that appear to be investing contrary to those policies.

The investment managers are incentivised to maintain an approach consistent with that when they were appointed by the Trustees by the payment of the investment management fee (and in the knowledge that a change of approach may cause investors to reconsider the investment).

The Trustees expect investment managers, where appropriate, to make decisions based on assessments of the longer term financial and non-financial performance of debt/equity issuers, and to engage with issuers to improve their performance. The Trustees assess this when selecting and monitoring managers.

Duration of Investment Manager Arrangements

Although the Trustees review the ongoing suitability of the pooled funds held regularly, the expectation is that pooled funds will normally be held for several years.

AVCs

AVCs are held separately from the Scheme’s other investments and the AVCs are used to secure benefits on a money purchase basis for members at retirement. From time to time the Trustees review the ongoing suitability of the AVC arrangements.

In assessing the suitability of a pooled fund, the Trustees consider, in conjunction with the Investment Adviser, how the fund would fit within the Scheme’s investment strategy and how the fund is expected to help the Trustees meet their investment objectives. As part of this consideration, all matters which are deemed to be financially material are taken into account including:

*This includes engaging with an issuer of debt or equity regarding matters including (but not limited to) performance, strategy, capital structure, management of actual or potential conflicts of interest, risks, and ESG considerations. It also includes engaging on these matters with other investment managers, other holders of debt or equity and persons or groups of persons who have an interest in the issuer of debt or equity.

At least every three years, the Trustees will review whether the ongoing use of each fund remains consistent with their investment strategy.

The Trustees will ensure any new pooled funds introduced into the investment strategy are appropriate to the circumstances of the Scheme.

The Trustees review the Scheme’s investments for all matters considered to be financially material (including ESG matters) regularly. This includes reviewing that each fund continues to operate in a manner that is consistent with the factors used by the Trustees to select the fund and that the choice of funds remains appropriate.

When assessing the performance of a fund, the Trustees do not usually place too much emphasis on short-term performance although they will seek to ensure that reasons for short-term performance (whether favourable or unfavourable) are understood.

To assist with the monitoring of the investment managers, the Trustees receive regular information from the Investment Adviser providing details of investment manager performance and asset allocation decisions. This analysis includes comparisons with benchmarks and relevant peer-group data. The analysis also assesses whether performance has been in line with expectations given market conditions and whether the level of risk has been as expected.

The Investment Adviser also provides regular updates on the investment managers’ actions regarding ESG matters and shareholder engagement.

The Investment Adviser regularly meets with the managers of pooled funds on its approved list.

In monitoring portfolio turnover costs for a pooled fund, the Trustees expect investment managers to provide cost data under the framework developed by the Cost Transparency Initiative.

Action when a pooled fund is causing concern

Where concerns about a fund are identified, the Trustees may look to reduce exposure to that fund or disinvest from it entirely. However, such action is expected to be infrequent, and, in the first instance, the Trustees would normally expect the Investment Adviser to raise the concerns with the investment manager. Thereafter, the Trustees, in conjunction with the Investment Adviser, would monitor the position to assess whether the situation improves.

The Trustees will regularly assess the ongoing suitability of each pooled fund held for all matters deemed to be financially material (including ESG matters and portfolio turnover costs).

The Trustees’ policy in relation to the exercise of rights attaching to investments and undertaking engagement activities in respect of investments is that they wish to encourage best practice in terms of stewardship.

However, because the Scheme’s assets are invested in pooled funds, the Trustees accept that ongoing engagement with the underlying companies (including the exercise of voting rights) will be determined by the investment managers’ own policies on such matters. The Trustees consider policies on engagement and voting in making decisions about retaining and appointing investment managers.

As a result of the use of pooled funds, the Trustees recognise that their ability to directly influence the action of companies is limited. Where the Trustees are unhappy with a manager’s engagement and / or voting, then in the first instance they would discuss this with the manager. Should this not resolve the Trustees’ concerns, then ultimately the Trustees may choose to disinvest.

The Trustees recognise that members might wish the Trustees to engage with the underlying companies in which the Scheme invests with the objective of improving corporate behaviour to benefit the environment and society. However, the Trustees’ priority is to select investment managers which are best suited to help meet the Trustees’ investment objectives, and ultimately to ensure that members’ benefits can be paid as and when they fall due. In making this assessment, the Trustees will receive advice from the Investment Adviser.

The Trustees recognise that investment managers’ engagement policies are likely to be focussed on environmental or societal benefits largely to the extent that these are consistent with maximising financial returns and minimising financial risks.

Nevertheless, the Trustees expect that each investment manager should discharge its responsibilities in respect of investee companies in accordance with that investment manager’s own corporate governance policies and current best practice, such as the UK Stewardship Code and the UN Principles for Responsible Investment.

The Trustees expect that, where appropriate, each investment manager should take ESG considerations into account when exercising the rights attaching to investments and in taking decisions relating to the selection, retention and realisation of investments.

The Trustees expect that the investment managers selected to manage the Scheme’s assets should invest for the medium to long term and should engage with issuers of debt or equity with a view to improving performance over this time frame.

The Trustees will review the stewardship policies of the investment managers on an annual basis.

The principal investment risks identified by the Trustees are listed below together with an explanation of how they are mitigated.

Indirect credit risk

The risk that an investment held within a pooled fund will suffer a financial loss because of a third party failing to pay monies that it owes.

Currency risk

The risk that the value of an investment will fall because of adverse movements in currency markets.

Real return risk

The risk that the Scheme’s assets do not deliver a long-term return in excess of inflation.

ESG risk

The risk that ESG factors will adversely impact the value of the Scheme’s investments.

Investment manager risk

The risk that an investment manager does not deliver returns in line with expectations.

Mitigation of the above risks

The risks listed above are mitigated by the Trustees monitoring the suitability of the pooled funds used by the Scheme. This monitoring is carried out in conjunction with the Investment Adviser.

Solvency and employer covenant risk

The risk that the Scheme’s assets fall short of the amount required to pay all benefits and expenses as they fall due and that insufficient assets could be recoverable from the sponsoring employer to meet the shortfall.

Mitigation

The Trustees’ funding approach is designed to be prudent and, in determining the funding and investment strategy, the Trustees consider the strength of the covenant of the sponsoring employer.

Self-Investment risk

The risk that the Scheme’s assets are linked to the sponsoring employer which could mean a reduction in the covenant of the sponsoring employer would simultaneously decrease the value of the Scheme’s assets.

Mitigation

The Trustees will ensure exposure to employer-related assets does not exceed limits prescribed in legislation.

Direct credit risk

The risk that disruption with an investment manager (such as fraud or insolvency) could adversely impact the value of the Scheme’s investments.

Mitigation

Any pooled funds held are structured such that the Scheme’s assets are ringfenced from the assets of the investment manager and other investors.

There are a number of mitigants in relation to fraud, including the investment managers’ internal controls.

Interest rate risk and inflation risk

The risk that movements in interest rates/expectations for future inflation will adversely impact the value of the Scheme’s investments.

Mitigation

Any assets held which have significant interest rate/inflation exposure will be selected to offset the sensitivity of the Scheme’s liabilities to interest rate/inflation movements. This approach mitigates interest rate risk and inflation risk.

Market Risk

The risk that the Scheme’s assets do not deliver a sufficient return, because of falls in investment markets.

Mitigation

The Trustees have an investment approach which is diversified across different asset classes.

Liquidity Risk

The risk that assets cannot be realised for cash when required.

Mitigation

The Trustees will invest the majority of the Scheme’s investments in funds which can be realised for cash at relatively short notice without incurring high costs. However, the Trustees recognise that the Scheme’s liabilities are long-term in nature and that a modest allocation to less-liquid investments may be appropriate.

Operational Risk in relation to LDI

The risk that sufficient cash cannot be passed across sufficiently quickly to recapitalise the Scheme’s LDI investments.

Mitigation

The Trustees have an automatic rebalancing arrangement in place and the platform provider is instructed to pass across the required cash automatically without the need for further Trustee intervention. The Trustees monitor the amount in the funds that are used in the automatic rebalancing arrangement.

The Trustees will:

The Trustees will review this statement at least every three years and without delay after any significant change in circumstances or investment strategy.

The Trustees will consult with the sponsoring employer before amending this statement.

The Trustees will obtain and consider written advice from the Investment Adviser before amending this statement.

The principles set out in this Statement have been agreed by the Trustees:

Signed:…………………………………………………… Date: ………………………

For and on behalf of the Trustees of the Jockey Club Racecourses Pension Scheme.

Appendix: The Trustees’ Investment Strategy

Strategic Asset Allocation

In determining the strategic asset allocation, the Trustees view the investments as falling into two broad categories:

At the time of agreeing the investment strategy, the strategic split of the Scheme’s assets between Growth and Liability Matching Assets was 68% Growth and 32% Liability Matching. This split is not regularly rebalanced and will fluctuate over time as market conditions change.

The strategic allocation for the Growth Assets is as follows:

|

Asset Class |

Current (as % of growth assets) |

Current (as % of total assets) |

|

Alternatives |

16% |

11% |

|

Equities |

32% |

22% |

|

Diversified Credit Funds |

52% |

36% |

|

Total Growth Assets |

100% |

68% |

The strategic allocation for the Liability Matching Assets is as follows:

|

Asset Class |

Current (as % of matching assets) |

Current (as % of total assets) |

|

LDI |

90% |

29% |

|

Corporate Bonds |

10% |

3% |

|

Total Liability Matching Assets |

100% |

32% |

The Liability Matching Portfolio is currently designed to match approximately 89% of the sensitivity of the Statutory Funding Objective liabilities to changes in gilt yields and inflation, but this may be reviewed in light of changes to market conditions and/or the Scheme's funding level.

In addition, the Trustees may hold cash in the Trustees’ bank account – particularly if it is to be used to make payments due in the short-term.

The allocation of the Growth Assets is not automatically rebalanced but will be monitored and rebalanced at the discretion of the Trustees. The strategic split by fund is in the Scheme’s Investment Implementation Policy.

|

ESG |

Environmental, Social and Governance |

|

Investment Adviser |

First Actuarial LLP |

|

L&G |

Legal & General Investment Management |

|

Scheme |

Jockey Club Racecourses Pension Scheme |

|

Scheme Year |

01 August 2024 to 31 July 2025 |

|

SIP |

Statement of Investment Principles |

|

UNPRI |

United Nations Principles for Responsible Investment |

This Implementation Statement reports on the extent to which, over the Scheme Year, the Trustees have followed their policy relating to the exercise of rights (including voting rights) attaching to the Scheme’s investments. In addition, the Implementation Statement summarises the voting behaviour of the Scheme’s investment managers and includes details of the most significant votes cast and the use of the services of proxy voting advisers.

In preparing this statement, the Trustees have considered guidance from the Department for Work & Pensions which was updated on 17 June 2022, as well as the expectations set out in the General Code of Practice.

The Scheme’s assets are invested in pooled funds and some of those funds include an allocation to equities. Where equities are held, the investment manager has the entitlement to vote.

At the end of the Scheme Year, the Scheme invested in the following funds which included an allocation to equities:

The Partners Fund (Guernsey) typically has an allocation of only 10-15% in listed equities and accounted for only 11% of the Scheme portfolio at 31 July 2025. This equity allocation therefore accounts for less than 2% of the Scheme’s overall portfolio. This is not considered to be significant by the Trustees and the Partners Fund (Guernsey) has not been included in the following analysis.

The Trustees’ policy in relation to the exercise of rights (including voting rights) attaching to the investments is set out in the SIP. The SIP was updated during the Scheme year to reflect changes made to the Scheme’s investment strategy, but wording relating to the exercise of rights was not revised. A summary of this wording is as follows:

The Trustees’ opinion is that their policy relating to the exercise of rights (including voting rights) attaching to the investments has been followed during the Scheme Year. In reaching this conclusion, the following points were taken into consideration:

*Note the voting analysis was over the year ending 30 June 2025 because this was the most recent data available at the time of preparing this statement. The Trustees are satisfied that the analysis provides a fair representation of the investment managers voting approach over the Scheme Year.

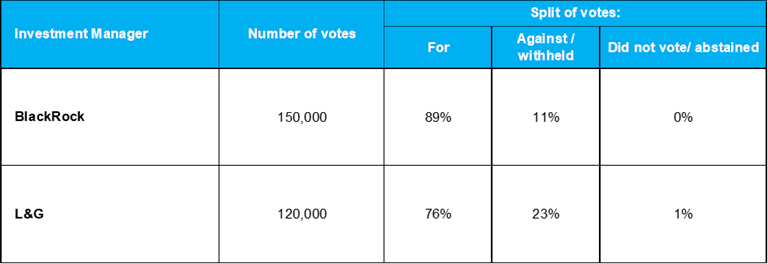

A summary of the investment managers’ records is shown in the table below.

Notes

These voting statistics are based on each manager’s full voting record over the 12 months to 30 June 2025 rather than votes related solely to the funds held by the Scheme.

The Trustees have reviewed the voting behaviour of the investment managers by considering the following:

The Trustees have also compared the voting behaviour of the investment managers with their peers over the same period.

Further details of the approach adopted by the Trustees for assessing voting behaviour is provided in the Appendix.

The Trustees’ key observations are set out below.

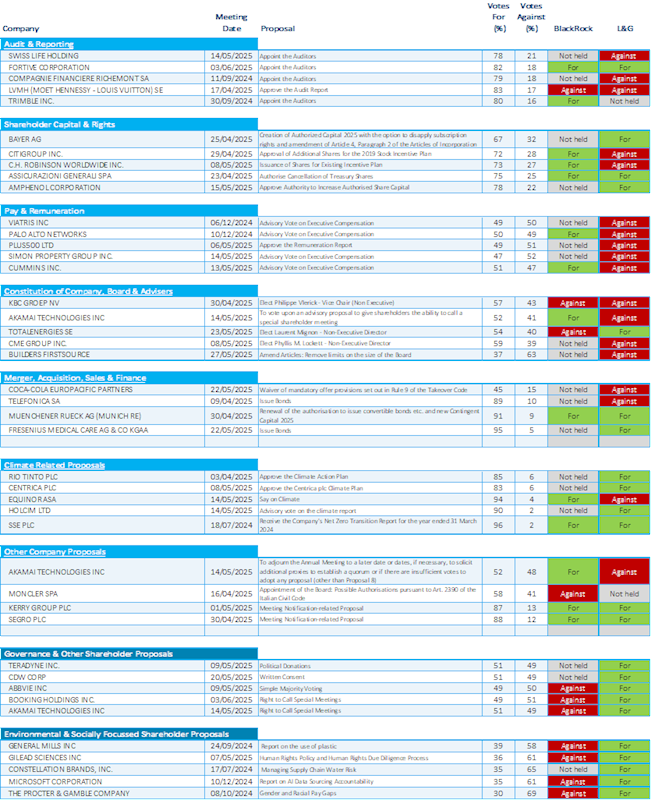

Based on information provided by the Trustees’ Investment Adviser, the Trustees have identified significant votes in nine separate categories. The Trustees consider votes to be more significant if they are closely contested. i.e. close to a 50:50 split for and against. A closely contested vote indicates that shareholders considered the matter to be significant enough that it should not be simply “waved through”. In addition, in such a situation, the vote of an individual investment manager is likely to be more important in the context of the overall result.

The five most significant votes in each of the nine categories based on shares held by the Scheme’s investment managers are listed in the Appendix. In addition, the Trustees considered each investment manager’s overall voting record in significant votes (i.e. votes across all stocks not just the stocks held within the funds used by the Scheme).

The Net Zero Asset Managers initiative (“NZAM”) brings together asset managers committed to the goal of achieving net-zero greenhouse gas emissions by 2050 as per the Paris Climate Agreement. In January 2025, following announcements of some managers exiting the agreement, NZAM announced a review of their overarching policies, which is ongoing.

The Trustees have considered their investment managers’ approach to NZAM as part of this analysis.

The Trustees recognise that analysis of BlackRock’s latest voting data has once again identified the manager to be generally unsupportive of shareholder proposals aimed at addressing ESG issues. This is further reflected by the manager’s decision to withdraw from NZAM.

L&G

The Trustees note that L&G’s voting record continues to compare very favourably with its peers.

As in previous years, analysis of L&G’s voting record identifies clear evidence that the manager is supportive of shareholder proposals designed to tackle ESG matters and is willing to vote against company directors on a broad range of issues. It is unsurprising that the manager has committed to remaining a member of NZAM, irrespective of the review’s outcome.

Based on the analysis undertaken, the Trustees have no concerns regarding the voting records of L&G.

The Trustees will keep the voting actions of BlackRock under review, particularly noting that in some instances there are areas that could still be improved.

The table below records how the Scheme’s investment managers voted in the most significant votes identified by the Trustees.

Note

In the table above, reliance is placed on periodic stock holding information to identify votes relevant to the Scheme. This means it is possible that some of the votes listed above may relate to companies that were not held within a pooled fund at the date of the vote. Equally, it is possible that there are votes not included above which relate to companies that were held within a fund at the date of the vote.

The Scheme did not hold certain companies where vote proposals were deemed to be significant, hence some of the rows in the table above are blank.

The methodology used to identify significant votes for this statement uses an objective measure of significance: the extent to which a vote was contested - with the most significant votes being those which were most closely contested.

The Trustees believe that this is a good measure of significance because, firstly, a vote is likely to be contentious if it is finely balanced, and secondly, in voting on the Trustees’ behalf in a finely balanced vote, an investment manager’s action will have more bearing on the outcome.

If the analysis were to rely solely on identifying closely contested votes, there is a chance many votes would be on similar topics which would not help to assess an investment manager’s entire voting record. Therefore, the assessment incorporates a thematic approach; splitting votes into nine separate categories and then identifying the most closely contested votes in each of those categories.

A consequence of this approach is that the number of significant votes is large. This is helpful for assessing a manager’s voting record in detail but it presents a challenge when summarising the significant votes in this statement. Therefore, for practical purposes, the table on the previous page only includes summary information on each of the significant votes.

The Trustees have not provided the following information which DWP’s guidance suggests could be included in an Implementation Statement:

The Trustees are satisfied that the approach used ensures that the analysis covers a broad range of themes and that this increases the likelihood of identifying concerns about a manager’s voting behaviour. The Trustees have concluded that this approach provides a more informative assessment of an investment manager’s overall voting approach than would be achieved by analysing a smaller number of votes in greater detail.

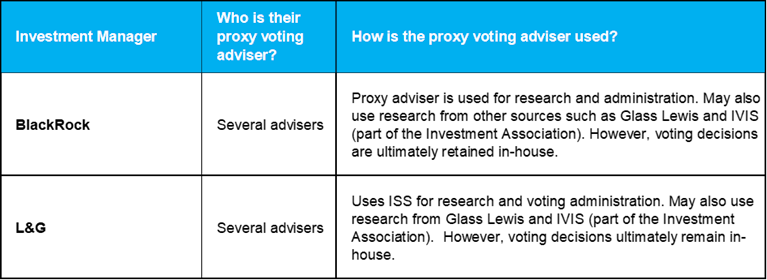

For more information concerning the investment managers’ voting policies and rationales, please visit the below links.

In accordance with the requirements of the Occupational Pension Schemes (Charges and Governance) Regulations 2015 (‘the Regulations’), the Trustees are required to provide a statement relating to the governance of the defined contribution (‘DC’) benefits held within the Scheme. This statement covers the period from 1 August 2024 to 31 July 2025 and has been prepared by the Trustees.

In the Scheme there are two different sets of members who hold benefits on a DC basis:

The Scheme is a defined benefit (‘DB’) arrangement which means that the benefits are calculated on a pre-determined basis specified in the Scheme Rules. The Scheme was contracted out using the protected rights method in respect of service accrued after 6 April 1997 (providing each member with an individual protected rights account). These Protected Rights accounts acted as an underpin to the defined benefits payable under the Scheme Rules.

Where members had less than two years’ service and received a refund of contributions prior to 6 April 2012, their protected rights accounts were retained within the Scheme and form a DC only benefit, as at that time it was not possible to provide a return of contributions in respect of their protected rights contributions.

Following the abolition of protected rights on 6 April 2012, the Trustees made a resolution in June 2012 which converted members’ protected rights funds into individual accumulation funds which act in the same way as non-protected rights funds but also continue to provide an underpin to their post 1997 benefits.

Therefore, in the Scheme there are some members with individual accumulation funds only and others where the individual accumulation fund acts as an underpin to DB benefits.

Where it acts as an underpin, upon retirement, death or transferring out of the Scheme, the value of the defined benefit is checked against the value of the individual accumulation funds and the higher benefit is provided to the member.

In addition to those members with individual accumulation fund accounts, all members could pay AVCs on a DC basis to provide additional benefits at retirement.

The Scheme currently offers a range of AVC investment choices with both Utmost Life and Pensions (‘Utmost’) and Royal London Mutual Insurance Society Limited (‘Royal London’).

Governance of the Default Investment Arrangement for the Individual accumulation funds

There is no default investment arrangement as defined in the Occupational Pension Schemes (Investment) Regulations 2005.

The Scheme has never been used as a Qualifying Scheme for meeting automatic enrolment obligations by the Principal Employer. Contributions to the Scheme, and therefore accrual within the individual accumulation fund accounts ceased on 31 March 2012. The assets in relation to the individual accumulation funds are invested within the Scheme’s DB assets and have been since 6 April 1997, and returns for all individual accumulation funds accrued in the Scheme from 6 April 1997 are based on the notional returns on the FTSE All Share Total Return Index.

Charges and Transaction Costs for the Individual accumulation funds

The investment returns on the Scheme’s DB assets considers the annual fund management charges of between 0.12% pa to 1.50% pa depending on the investment fund. However, members with individual accumulation funds have notional holdings in the DB scheme and for the purposes of the valuation of these benefits, assumed investment growth is linked to the FTSE All Share Total Return Index and an allowance for investment expenses of 0.50% pa is made.

These charges are incurred by members when valuing their individual accumulation funds to assess whether the underpin bites.

Cumulative costs and charges for the Individual accumulation funds

The Trustees have conducted an analysis of the cumulative impact of the member-borne costs and charges for a typical member of the Scheme invested in the individual accumulation funds, which is set out in the Appendix A.

Net Investment Returns for the Individual accumulation funds

The following table reflects the performance of the fund over varying periods based on investment after charges have been deducted and has considered the statutory guidance.

|

Fund |

% Annualised Performance to 31 July 2025 |

||

|

1 year |

3 years p.a. |

5 years p.a. |

|

|

Individual accumulation funds |

11.6 |

10.1 |

12.2 |

Value for Members for the Individual accumulation funds

Under the Occupational Pension Schemes (Administration, Investment, Charges and Governance) (Amendment) Regulations 2021, trustees of ‘specified schemes’ providing DC benefits are required to carry out an assessment of their scheme’s value for members.

Following the Department for Work & Pensions (‘DWP’) guidance, an assessment of value for members has been carried out in respect of the individual accumulation fund accounts which considered the following aspects:

As part of the assessment process the costs and charges and net investment performance must be benchmarked against three alternative large modern pension arrangements. The Trustees benchmarked the costs and charges and net investment performance against The People’s Pension Master Trust, Now:pensions Master Trust and Smart Pension Master Trust.

Looking at the costs and charges, the DC benefits of the Scheme are higher than those quoted by three comparator DC pension providers who also include administration services within their Annual Management Charges.

It should however be noted that whilst they have provided indicative terms, they are unable to accept benefits from the scheme given the underpins that exist.

Looking at net investment returns using the returns on the FTSE All Share Total Return Index, on which investment returns of the individual accumulation funds are based, when reviewed against the other comparator schemes used in the assessment, the individual accumulation funds delivered higher returns over three and five year periods. Over 12 months, the individual accumulation funds were ahead of two of the three alternative providers and marginally behind the highest performing provider.

There are some other areas where improvements could be made when considering Governance and Administration.

These relate to:

Overall, our assessment concludes that the DC benefits do not meet the requirements laid down by The Pensions Regulator (‘the Regulator’).

There are certain changes that can be made that are simple and practical to implement which we have noted above.

We are mindful that the Regulator expects member outcomes to be improved where their standards are not met. We have taken a number of steps to explore alternative remedies. The reality is that for a small value of funds, where the underpin exists and where no new monies are being added, providers are unable or unwilling to offer suitable alternative and better arrangements. We will continue to review and seek to improve the current arrangements as far as is possible.

In September 2025 the Chair of Trustees had correspondence with the Regulator whereby the Trustees’ 2024 Value for Member assessment process and conclusions, alongside details of the structure of the Scheme, was relayed to the Regulator. The Regulator noted the information and had no further questions.

Governance of the Default Investment Arrangement for the AVCs

The deemed default investment arrangements for the AVCs as defined in the Regulations are:

The Cautious Lifestyle Strategy (Annuity) became a deemed default investment arrangement when the investment option changed from the Cautious Retirement Investment Strategy in 2021, as part of a review which Royal London conducted on its legacy strategies.

The Investing by Age became a deemed default investment arrangement when the Equitable Life With Profits Fund was closed from 1 January 2020. Members who were invested in the With Profits fund had their fund holdings switched to the Secure Cash fund for the first 6 months and then into the Investing at Age Strategy with effect from 1 July 2020.

The Trustees considered the appropriateness of the current AVC arrangements in November 2025, as well as the options available. This review was undertaken in the knowledge that most members use their AVC funds as the first option to provide additional tax-free cash at retirement. The Trustees concluded that no changes needed to be made at this time.

There were no specified performance-based fees incurred in relation to the deemed default investment arrangements during the Scheme year.

The Trustees have prepared a Statement of Investment Principles (‘SIP’) which sets out the Trustees’ aims and objectives relating to the Defined Benefit investment strategy. This was last updated in June 2025. A copy of the SIP can be found at https://www.thejockeyclub.co.uk/defined-benefit-pension-scheme/.

The asset allocation of the Royal London Cautious Lifestyle Strategy (Annuity) across a range of age profiles as at 31 July 2025 is shown in the table below and has taken account of the statutory guidance.

|

Asset Allocation on 31 July 2025 |

% Allocation for an average 25-year-old |

% allocation for an average 45-year-old |

% allocation for an average 55-year-old |

% allocation for an average person, 1 day before SPA* |

|

Cash |

1.7 |

3.2 |

6.9 |

1.9 |

|

Bonds |

11.4 |

36.9 |

64.4 |

86.2 |

|

Listed Equity |

70.8 |

45.0 |

18.8 |

0.3 |

|

Private Equity |

0.0 |

0.0 |

0.0 |

0.0 |

|

Infrastructure |

0.0 |

0.0 |

0.0 |

0.0 |

|

Property |

11.1 |

9.9 |

4.9 |

0.0 |

|

Private Debt |

0.0 |

0.0 |

0.0 |

0.0 |

|

Other |

5.0 |

5.0 |

5.0 |

11.6 |

* State pension age

The asset allocation of the Utmost Investing by Age Strategy (Annuity) across a range of age profiles as at 30 June 2025 is shown in the table below and has taken account of the statutory guidance.

|

Asset Allocation on 30 June 2025 |

% Allocation for an average 25-year-old |

% allocation for an average 45-year-old |

% allocation for an average 55-year-old |

% allocation for an average person, 1 day before SPA* |

|

Cash |

6.2 |

6.2 |

6.2 |

7.0 |

|

Bonds |

36.0 |

36.0 |

36.0 |

58.7 |

|

Listed Equity |

57.2 |

57.2 |

57.2 |

33.8 |

|

Private Equity |

0.0 |

0.0 |

0.0 |

0.0 |

|

Infrastructure |

0.0 |

0.0 |

0.0 |

0.0 |

|

Property |

0.0 |

0.0 |

0.0 |

0.0 |

|

Private Debt |

0.0 |

0.0 |

0.0 |

0.0 |

|

Other |

0.6 |

0.6 |

0.6 |

0.5 |

* State pension age

Charges and Transaction Costs for the AVCs

The total expense ratio for the Royal London funds is 0.53% per annum and this is made up of an annual management charge and other indirect costs.

In addition to these explicit member charges, members may also incur transaction costs (incurred when buying, selling, lending or borrowing investments). The transaction costs for the Royal London funds are calculated to 31 December 2024.

The Royal London Cautious Retirement Investment Strategy (Annuity) is a lifestyle strategy. The ranges which members would experience are shown in the table below and are based on a member with a target retirement age of 65:

|

Age |

% Charges p.a. (Total Expense Ratio) |

% Transaction Costs p.a.

|

% Total Costs and Charges p.a. |

|

<50 |

0.53 |

0.14 |

0.67 |

|

50 to 54 |

0.53 |

0.10 to 0.14 |

0.63 to 0.67 |

|

55 to 59 |

0.53 |

0.05 to 0.10 |

0.58 to 0.63 |

|

60 to 64 |

0.53 |

0.05 to 0.09 |

0.58 to 0.62 |

|

65+ |

0.53 |

0.09 |

0.62 |

On 18 November 2024, Royal London updated the names of their Governed Portfolios to make them easier to understand. There were no changes to any of the underlying investments or how they’re managed. For more information on these changes, please visit: https://www.royallondon.com/pensions/investment-options/fund-changes/.

The following tables shows the total costs and charges for the funds with Royal London.

|

Royal London Fund |

% Charges p.a. (Total Expense Ratio) |

% Transaction Costs p.a.

|

% Total Costs and Charges p.a. |

|

Governed Portfolio Enhanced |

0.53 |

0.14 |

0.67 |

|

Governed Portfolio Moderate |

0.53 |

0.10 |

0.63 |

|

Governed Portfolio Defensive |

0.53 |

0.05 |

0.58 |

|

Deposit |

0.53 |

0.00 |

0.53 |

|

Managed |

0.53 |

0.12 |

0.65 |

|

With Profits |

0.53 |

0.13 |

0.66 |

The Utmost funds are subject to an ongoing investment management charge. In addition to these explicit member charges, members may also incur transaction costs (incurred when buying, selling, lending or borrowing investments). The transaction costs for Utmost funds are to 30 June 2025.

The Utmost Investing by Age Strategy is a lifestyle strategy. The ranges which members would experience are shown in the table below and are based on a member with a target retirement age of 65.

|

Age |

% Charges p.a. (Total Expense Ratio) |

% Transaction Costs p.a.

|

% Total Costs and Charges p.a. |

|

<55 |

0.75 |

0.35 |

1.10 |

|

55 to 64 |

0.75 |

0.35 to 0.39 |

1.10 to 1.14 |

|

65 to 74 |

0.75 |

0.39 |

1.14 |

|

75+ |

0.50 to 0.75 |

0.01 to 0.39 |

0.51 to 1.14 |

The following tables summarise the total costs and charges for the funds available on self-select basis with Utmost.

|

Utmost Fund |

% Charges p.a. (Total Expense Ratio) |

% Transaction Costs p.a.

|

% Total Costs and Charges p.a. |

|

Multi Asset Moderate |

0.75 |

0.35 |

1.10 |

|

Multi Asset Cautious |

0.75 |

0.39 |

1.14 |

|

Managed |

0.75 |

0.17 |

0.92 |

|

UK Equity |

0.75 |

0.20 |

0.95 |

|

Clerical Medical With-Profits* |

0.50 |

0.24 |

0.74 |

* The total expense ratio is implicit in the bonus rate set for the current year.

The total expense ratio for the Clerical Medical With-Profits fund is considered when declaring annual interest rates rather than being an explicit charge deducted from members’ funds.

Members are also eligible to receive a final bonus at maturity. The amount of the final bonus may be lower, or nil, on transfer or encashment before maturity. A market value reduction may be applied to the With Profits Fund on transfer or encashment before maturity. This ensures that members who choose to leave the fund before their normal retirement date do so on terms that properly reflect the underlying value of their policy.

Cumulative costs and charges for the AVCs

The Trustees have conducted an analysis of the cumulative impact of the member-borne costs and charges for a typical member of the Scheme invested in the deemed default investment strategies, which is set out in the Appendix B.

The Trustees have not provided illustrations of the cumulative impact of the member-borne costs and charges for the self-select AVC arrangements as these are not considered significant in relation to the overall investments of the Scheme and it would therefore be disproportionate.

Net Investment Returns for the AVCs

All information shown reflects the performance of the strategies/funds over varying periods based on investment after charges have been deducted and has considered the statutory guidance.

The net investment returns for members invested in the Royal London Cautious Lifestyle Strategy (Annuity) will vary for members at different ages. The table below shows age-related returns at ages 25, 45 and 55, based on a member with a target retirement age of 65:

|

% Age Related Returns to 31 July 2025 |

||||

|

Age |

1 year |

3 years p.a. |

5 years p.a. |

10 years p.a. |

|

25 |

8.3 |

6.0 |

7.1 |

6.1 |

|

45 |

8.3 |

6.0 |

7.1 |

6.1 |

|

55 |

7.0 |

4.6 |

5.2 |

5.2 |

The following table shows the net investment performance of the Royal London self-select funds.

|

% Annualised returns to 31 July 2025 |

||||||

|

Royal London Fund |

1 year |

3 years p.a. |

5 years p.a. |

10 years p.a. |

15 years p.a. |

20 years p.a. |

|

Governed Portfolio Enhanced |

8.3 |

6.0 |

7.1 |

6.1 |

7.2 |

6.4 |

|

Governed Portfolio Moderate |

7.0 |

4.6 |

5.2 |

5.2 |

n/a |

n/a |

|

Governed Portfolio Defensive |

5.2 |

2.2 |

1.6 |

3.1 |

n/a |

n/a |

|

Annuity |

1.5 |

0.3 |

-1.1 |

n/a |

n/a |

n/a |

|

Deposit |

4.4 |

4.1 |

2.4 |

1.2 |

0.8 |

1.5 |

|

Managed |

7.9 |

6.3 |

7.6 |

6.2 |

7.1 |

6.3 |

|

With Profits* |

n/a |

n/a |

n/a |

n/a |

n/a |

n/a |

* Royal London have not been able to provide net investment returns for their With Profit Fund. The total investment return applied to asset shares in the With Profits Fund (before taxes and charges) for 2024 was 10.6%. Regular annual bonuses are added to members’ policies, and a final bonus may also be payable. In 2024, an annual bonus of 3.15% was added, which includes a ProfitShare Bonus of 0.15%.

The net investment returns for members invested in the Investing by Age Strategy will vary at different ages. Up to age 55, members are fully invested in the Multi Asset Moderate Fund and therefore the returns at ages 25, 45 and 55 will be the same.

|

% Age Related Returns to 31 July 2025 |

||||

|

Age |

1 year |

3 years p.a. |

5 years p.a. |

|

|

25 |

9.1 |

7.4 |

6.9 |

|

|

45 |

9.1 |

7.4 |

6.9 |

|

|

55 |

9.1 |

7.4 |

6.9 |

|

The following table shows the net investment performance of the Utmost self-select funds.

|

% Annualised returns to 31 July 2025 |

|||

|

Utmost Fund |

1 year |

3 years p.a. |

5 years p.a. |

|

Multi Asset Moderate |

9.1 |

7.4 |

6.9 |

|

Multi Asset Cautious |

6.1 |

3.6 |

2.1 |

|

Money Market |

4.3 |

4.1 |

2.3 |

|

Managed |

10.0 |

8.1 |

8.3 |

|

UK Equity |

13.1 |

11.0 |

12.2 |

|

Clerical Medical With-Profits* |

n/a |

n/a |

n/a |

*We have been unable to obtain net investment returns or annual bonus rates for the Clerical Medical With-Profits Fund. The annualised 5-year return of the underlying assets (i.e. unsmoothed) is 3.6% to 31 December 2024.

The Trustees receive and review reports from the Scheme’s administrators on at least a 6-monthly basis to monitor the level of administration services being provided to members.

The processing of core financial transactions is monitored by the administrators, who have implemented internal control procedures to help ensure that such transactions are processed promptly and accurately (including a relevant review process). These activities include procedures to ensure the accuracy of benefit calculations and settlements, and the prompt resolution of any inconsistencies identified. Activities covered include controls and procedures to manage the settlement of benefits and individual transfers out.

The Trustees are satisfied that during the period of this statement, transactions have been completely promptly and accurately.

It is important that the Trustees continue to have sufficient knowledge and understanding to fulfil their duties. This is complemented by having a professional trustee (Capital Cranfield Trustees) on the trustee board. All new Trustees are required to undertake training following their appointment, including use of the Pensions Regulator’s Trustee Toolkit. All Trustees have also been provided with and have a working knowledge of the Scheme’s documents including the Trust Deed and Rules, SIP and other informal policies.

The Trustees are supported by independent and professional advisers who ensure that they are kept abreast of the latest legislative, regulatory and market developments that apply to the Scheme. These advisory appointments are also periodically reviewed.

Training is delivered during Trustees’ meetings when the Trustees are considering issues, the understanding of which is enhanced through training. Relevant training materials are included in Trustees’ meeting packs.

All training received by the Trustees is recorded and the training needs of the Trustees are regularly reviewed by the Trustees and their advisers to identify any relevant gaps in knowledge.

The annual DC value for member assessment is an agenda item at the Trustees’ meeting. The Trustees have also received training on the value for member regulations.

The Trustees have received papers explaining the structure of the individual accumulation funds underpin, and also reviewing the AVC providers.

In addition, Capital Cranfield Trustees are subject to AAF audit requirements which require each of its professional trustees to attend a number of technical training sessions per year.

The Trustees have sufficient knowledge and understanding of the law relating to pensions and trusts, as well as sufficient knowledge and understanding of the relevant principles relating to the funding and investment of occupational schemes.

Overall, the Trustees’ combined knowledge and understanding, together with available advice, enables them to properly exercise their functions.

If you have any further queries regarding the Scheme, please contact:

First Actuarial LLP

2nd Floor

Mayesbrook House

Lawnswood Business Park

Leeds

LS16 6QY

Tel: 0113 818 7300

Email: leeds.admin@firstactuarial.co.uk

William Medlicott

Chair of the Trustees of the Jockey Club Racecourses Pension Scheme

The table below shows the cumulative impact of costs and charges (as set out in the main body of this Statement) for the Individual accumulation funds. They are presented in the format prescribed by legislation and on the specific assumptions outlined below.

Individual accumulation funds

|

|

Projected Pension Pot in today’s money |

|

|

Years |

Before charges |

After all costs and charges |

|

1 |

£21,333 |

£21,228 |

|

3 |

£22,016 |

£21,692 |

|

5 |

£22,720 |

£22,166 |

|

10 |

£24,581 |

£23,398 |

|

15 |

£26,594 |

£24,697 |

|

20 |

£28,773 |

£26,069 |

|

25 |

£31,130 |

£27,517 |

|

30 |

£33,679 |

£29,045 |

Individual accumulation fund 1.59% pa above inflation

The table below shows the cumulative impact of costs and charges (as set out in the main body of this Statement) for the Royal London Cautious Lifestyle Strategy and Utmost Investing by Age Strategy. They are presented in the format prescribed by legislation and on the specific assumptions outlined below.

|

|

Projected Pension Pot in today’s money |

|||

|

|

Royal London Cautious Lifestyle Strategy |

Utmost Investing by Age Strategy |

||

|

Years |

Before charges |

After all costs and charges |

Before charges |

After all costs and charges |

|

1 |

£21,656 |

£21,516 |

£21,501 |

£21,287 |

|

3 |

£23,031 |

£22,585 |

£22,538 |

£21,873 |

|

5 |

£24,494 |

£23,708 |

£23,626 |

£22,474 |

|

10 |

£28,569 |

£26,766 |

£26,580 |

£24,052 |

|

15 |

£33,322 |

£30,218 |

£29,903 |

£25,740 |

|

20 |

£38,328 |

£33,667 |

£33,642 |

£27,548 |

|

25 |

£42,297 |

£36,091 |

£37,634 |

£29,309 |

|

30 |

£44,244 |

£36,732 |

£41,508 |

£30,730 |

Royal London Enhanced 3.13% pa above inflation

Royal London Moderate 2.41% pa above inflation

Royal London Defensive 1.36% pa above inflation

Royal London Annuity 0.22% pa above inflation

Utmost Moderate 2.38% pa above inflation

Utmost Cautious 1.81% pa above inflation